Bittensor cut its emissions in half in December, and roughly 70% of the supply is locked in staking. The supply side looks tight, but a halving only moves price if demand shows up to meet it.

Summary

- Bittensor (TAO) ran its first halving on Dec. 12, 2025, cutting daily emissions from 7,200 to 3,600 TAO against a fixed 21 million cap, the same hard-cap design Bitcoin uses.

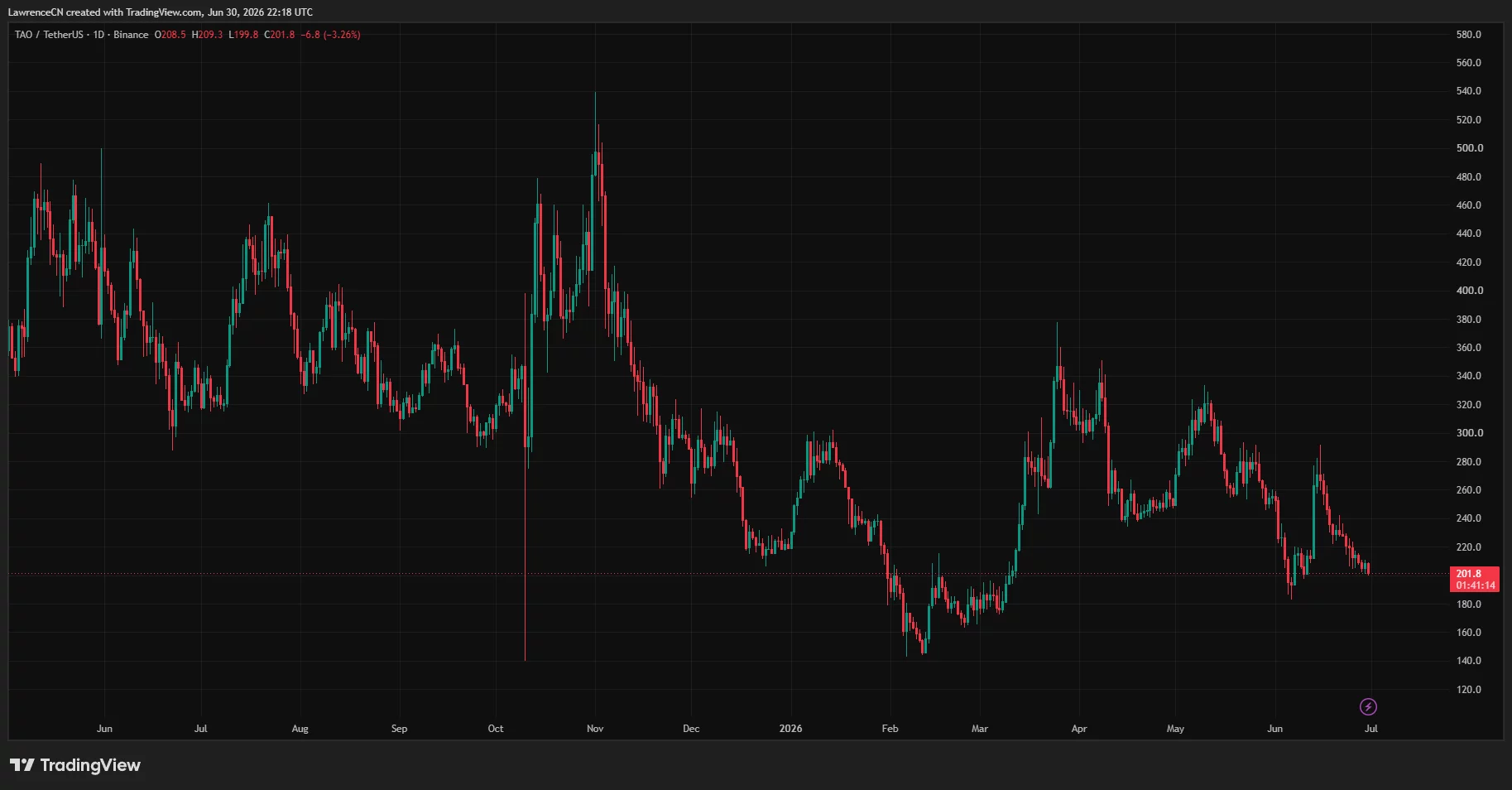

- TAO trades near $250 as of late June 2026, roughly 65% below its early-2024 record near $757, ranked around #27 to #37 with a market cap close to $3 billion and only about 11 million tokens in circulation.

- The bull case rests on a tightening float: with around 70% of supply staked for roughly 10% yield, the halved emissions slowly thin out sell-side pressure, which can lift price if demand holds or grows.

- The bear case is that a halving is a supply event the market already knew about, and TAO’s real problem is proving its subnets capture lasting value instead of riding AI-narrative momentum that fades.

- Analyst forecasts for 2026 run wide, from Gate near a $236 average to Coinpedia eyeing a $500 reclaim, with the outcome hinging on subnet revenue, ETF flows, and the broader AI trade more than on the halving alone.

Bittensor’s first halving is already in the past. It happened on Dec. 12, 2025, and the daily issuance of TAO dropped from 7,200 tokens to 3,600 overnight. So the live question for 2026 is not whether the halving will happen. It is what a halving actually does to a token whose price sits 65% below its record, whose technical picture is bearish, and whose deeper story is still unproven. The supply math is real. Whether it matters depends on demand, and that is the harder part of the forecast.

This piece walks through how the Bittensor halving works, why a supply cut takes months to filter into the market, the demand-side question the halving does not answer, what the charts say at current levels, the institutional wildcard around a possible spot ETF, and where analysts think TAO could trade in 2026. It closes with bull, base, and bear scenarios and a short FAQ.

How the Bittensor halving actually works

Bittensor is an open marketplace for machine intelligence. Models, compute, and data compete inside specialized markets called subnets, and the network scores their output through a mechanism known as Yuma Consensus.

TAO is the settlement token that pays for useful work and secures the network through staking. The protocol was started in 2019 by AI researchers Ala Shaabana and Jacob Steeves, and its token design borrows directly from Bitcoin: a fixed cap of 21 million coins and a halving schedule that cuts new issuance over time.

The December 2025 halving was the first of these events. Daily emissions fell from 7,200 TAO to 3,600. In plain terms, the network now mints half as much new TAO each day as it did before. Miners and validators who earn TAO for their contributions receive a smaller flow of new tokens, which over time means less fresh supply hitting the market. The mechanism is the same logic that underpins Bitcoin halvings, where reduced issuance has historically preceded periods of price strength, though the cause and effect is never as clean as the charts make it look in hindsight.

The key difference between a halving in theory and a halving in practice is timing. Issuance dropped instantly on the halving date, but the effect on circulating supply is gradual. The tokens already in circulation do not disappear, and the slower drip of new supply only changes the balance of buyers and sellers over weeks and months, not in a single candle. That is why the halving is better understood as a structural shift in the background rather than a switch that flips price higher on the day.

Why the supply cut takes months to bite

The most important number for the supply thesis is not the emission rate. It is how much TAO is locked away and cannot be sold. Roughly 70% of the circulating supply is staked by validators and delegators, who earn an annual yield in the region of 10% for securing the network. Staked tokens are not idle, but they are also not sitting on exchange order books waiting to be dumped. That combination, halved emissions plus a high staking ratio, is what makes the Bittensor float look unusually thin compared with most tokens of similar size.

Here is the chain of logic the bulls lean on. New supply has been cut in half. A large majority of existing supply is staked and earning yield, so holders are paid to keep it locked. If demand for TAO stays flat or rises while the liquid, sellable float shrinks, the price pressure shifts upward over time. This is the classic supply-shock argument, and on paper it is coherent. With only about 11 million of the 21 million cap in circulation and most of that staked, the genuinely tradable supply is a fraction of the headline number.

The honest caveat is that supply shocks are slow and conditional. The phrase doing the heavy lifting is “if demand stays flat or rises.” Reduced emissions cannot lift a price by themselves if buyers walk away faster than sellers do. Through the first half of 2026, that is roughly what happened: TAO slid toward $200 in early June before rebounding, even though the halving was months in the rearview mirror. The supply setup was already in place, and it did not stop the drawdown. The lesson is that the halving loads the spring, but something on the demand side has to pull the trigger.

The demand side the halving does not solve

This is the part of the forecast that actually decides where TAO goes, and it has nothing to do with the halving. Bittensor’s value depends on whether its subnets capture real, durable economic demand for machine intelligence, or whether TAO is mostly a high-beta proxy for AI enthusiasm that rises and falls with the narrative.

There is a real case to make. The subnet ecosystem has expanded past 120 active markets, each handling a specialized task such as inference, compute, data, or prediction. The network reported around $43 million in Q1 2026 revenue from AI services, which is a concrete sign that money is moving through the system instead of just speculation.

The Dynamic TAO, or dTAO, upgrade lets subnets allocate emissions based on real demand instead of fixed rewards, which is meant to price intelligence by the market and push Bittensor from a research project toward actual economic activity. The ambition is large: to be the settlement layer for intelligence itself, the place where models, compute, data, and incentives meet in one market.

The bear reading is that this is still unproven, and the network has shown it can break. In April 2026, a high-profile subnet exit triggered a roughly 25% price drop, exposing how much concentration and governance fragility sit underneath the optimistic story. The market punished the weak decentralization signal fast.

The deeper worry is value capture: even if subnets generate revenue, it is not yet clear how much of that value flows back to the TAO token itself rather than to the subnet operators or token holders downstream. An AI token can have busy subnets and still struggle to translate that activity into sustained token demand.

When AI excitement runs hot across the market, TAO tends to jump, and when attention rotates elsewhere, it tends to fade. That correlation is the bear case in one sentence: if TAO is mostly AI-hype beta, the halving will not save it.

What the charts say right now

At current levels near $250, TAO sits in a bearish-to-neutral technical posture. Through June, it traded below the cluster of 50-day, 100-day, and 200-day exponential moving averages sitting roughly between $256 and $270, which means the medium-term trend has been pointing down and that band overhead acts as resistance. Momentum readings have hovered in weak-to-neutral territory, with relative strength index values in the mid-30s to mid-50s depending on the day, not oversold enough to scream reversal and not strong enough to confirm one.

The levels traders watch are clear. On the downside, the $200 area has acted as a line in the sand through June, and a decisive break below it opens the door toward the February low near $163. On the upside, the first hurdle is reclaiming that $256 to $270 moving-average band, and above it the structure points toward $352 and then $396, the levels several analysts flag as the gateway to a larger move.

The longer-term chart frames the whole range: an accumulation floor around $160 to $200 and a distant ceiling near the $720 to $760 zone that produced the record in early 2024. TAO has cycled inside that channel before, finding demand at the lows and heavy profit-taking at the highs.

The takeaway from the charts is that TAO is not in a breakdown, but it is not in an uptrend either. It needs to reclaim its moving averages before the supply thesis gets any technical confirmation, and until it does, the halving narrative is a fundamental tailwind fighting a bearish trend.

The institutional wildcard

The most underpriced catalyst in the TAO forecast may be the one that has nothing to do with the chart. Grayscale filed an S-1 for a Bittensor trust on Dec. 30, 2025, and its Grayscale Bittensor Trust is already live over the counter, giving accredited investors a regulated wrapper for TAO exposure. Bitwise has also filed for a spot TAO product, with a U.S. regulatory decision expected around August 2026. The exact timing is not guaranteed, and approval is not certain, but the direction of travel matters.

The reason this is a wildcard rather than a sure thing is the corridor it opens. Once an asset is treated as ETF-eligible, it stops being dismissed as a pure speculation and starts being treated as infrastructure exposure that funds can hold without touching spot crypto directly. Bitcoin went through this in its earlier institutional phase, and Ethereum followed.

TAO is now entering the same corridor as the leading decentralized-AI asset. Anticipation alone can move price, because spot buyers tend to position early when future access looks credible.

There is a broader narrative tailwind too. When confidence in centralized AI wobbles, capital has flowed toward decentralized alternatives, and one such episode pushed an estimated $2.87 billion into AI crypto tokens inside a single week. TAO is the default beneficiary of that rotation given its position as the category leader by market cap. The flip side is that this same dependence on the AI narrative is exactly the fragility the bears point to: flows that arrive on a narrative can leave on one too.

What analysts forecast for TAO in 2026

Forecasts for TAO in 2026 span an enormous range, which is itself the honest signal: the outcome depends on variables no model can pin down. The figures below are third-party projections, presented as a spread of views, not as targets this publication endorses.

On the cautious end, Gate’s model centers 2026 around an average near $236, with a projected low close to $130 and a high around $318, essentially expecting TAO to hold near current levels with wide swings. Coindataflow’s experimental forecast sits in a similar low band, with a 2026 high near $281. In the middle and higher, Changelly’s analysis points to a 2026 range of roughly $388 to $472 with an average near $402, while Cryptopolitan’s technical read frames a $134 to $570 band with an average around $475.

Coinpedia takes a more constructive technical view, arguing that if TAO clears resistance at $352 and $396 in the 1st half of the year, the path opens toward a $500 reclaim. Looking further out, long-term projections from several of these firms cluster in a $900 to $3,000 range for 2030, premised on decentralized AI demand expanding and TAO holding its category lead.

The width of that spread, from a low near $130 to highs above $570 in the same year, is not a failure of analysis. It is an accurate reflection of how much hinges on whether subnet demand compounds, whether an ETF arrives, and whether the AI trade stays in favor. The halving sets the supply backdrop. These other forces decide the magnitude.

How the Bittensor halving compares with Bitcoin’s

The halving thesis borrows its emotional weight from Bitcoin, where four-year supply cuts have lined up with major bull runs. The comparison is useful, but it breaks down in ways that matter for the forecast. Bitcoin’s halving reduces the new supply paid to miners who secure a settlement network whose demand driver is, broadly, monetary: people want to hold Bitcoin as a store of value.

Bittensor’s halving reduces the new supply paid to miners and validators who produce and verify machine intelligence, and TAO’s demand driver is supposed to be usage of that intelligence through subnets. Those are different engines.

The practical consequence is that a Bittensor halving cannot lean on the same reflexive narrative. Bitcoin’s halvings work partly because a huge population of holders believes they work, which makes the belief partly self-fulfilling. TAO does not yet have that scale of conviction, and its price has shown it: the token fell after the December halving instead of rallying on it, because the AI-token market cared more about subnet performance and the broader risk environment than about a supply chart. The halving is real and structurally helpful, but anyone modeling TAO on a clean Bitcoin-style post-halving curve is importing an assumption the data has not yet earned.

There is also a proportionality difference. Bitcoin’s reduced issuance is a small fraction of its already-large circulating supply, so the supply effect is gradual while the narrative effect is immediate.

For TAO, the emission cut is proportionally larger against a much smaller circulating base, which should make the mechanical supply effect more potent over time, yet the narrative effect is weaker because fewer participants treat the halving as gospel. The net is a token where the fundamentals of the halving may matter more than they do for Bitcoin, while the storytelling matters less.

The deeper design point sits underneath all of this. Bittensor was built by Ala Shaabana and Jacob Steeves in 2019 around Yuma Consensus, the mechanism that scores and rewards useful machine-intelligence work. That design is what lets the network claim it pays for output instead of raw hardware uptime, and it is the foundation of the value-capture argument. The halving sharpens the supply side of that design, but it does not resolve whether the scoring turns into durable token demand, which remains the open question the price keeps asking.

What to watch through the rest of 2026

For readers tracking TAO instead of chasing headlines, a short list of signals will reveal which scenario is unfolding well before the price confirms it. The first is subnet revenue: the roughly $43 million reported for the first quarter is the number to watch for growth, because rising real revenue is the strongest evidence that the value-capture story is working instead of stalling. The Second is the moving-average band between $256 and $270; reclaiming and holding above it would be the first technical sign the bearish trend has turned.

The third is the ETF timeline, with a U.S. decision expected around August 2026. An approval, or even rising odds of one, would open the institutional corridor the bull case needs, while a denial or a delay removes a catalyst the market has started to anticipate.

The fourth is governance stability: after the April subnet exit that triggered a 25% drop, any repeat of concentration or governance trouble would confirm the fragility the bears emphasize and could undo months of recovery in days. The fifth is the health of the broader AI trade, since TAO has behaved as a high-beta proxy for AI sentiment, and a rotation out of AI tokens would pressure it regardless of its own progress.

Watched together, these five tell a more reliable story than any single price target. If subnet revenue climbs, the moving averages flip, and the ETF path advances, the supply setup from the halving finally has demand to work with, and the bull case gains real footing. If revenue stalls, governance wobbles, and the AI trade cools, the thin float will amplify the downside instead of cushioning it. The halving set the stage in December. These signals decide whether anyone shows up to use it.

Bull, base, and bear scenarios for TAO

The scenarios below combine the supply setup with the demand and institutional variables that actually drive the outcome. They are illustrative ranges built from the third-party forecasts above and current market structure, not guarantees.

Bull case

In the bull scenario, the halving thesis works as designed and demand shows up to meet the tightening float. Subnet revenue keeps climbing from the $43 million Q1 pace, dTAO routes emissions toward markets with real usage, and the value-capture question starts to resolve in TAO’s favor. A spot ETF decision lands favorably or looks likely, pulling regulated capital into a thin float where roughly 70% of supply is staked and out of reach. TAO reclaims the $256 to $270 moving-average band, breaks $352 and $396, and runs toward the $500 area that Coinpedia and others flag, with the more aggressive long-term models pointing higher into 2027 if the AI trade stays hot. This case depends on the AI narrative staying strong and the network avoiding another governance shock.

Base case

In the base scenario, the halving slowly does its quiet work but no single catalyst fires hard. Subnet activity grows unevenly, the ETF path advances but without a clean approval inside 2026, and the AI trade runs warm instead of euphoric. TAO spends the year chopping inside its broad trading channel, roughly between the $200 floor and the low-$400s, with the average landing near the $236 to $402 zone that the Gate and Changelly models bracket. The thin float keeps downside contained on dips, but the unproven value-capture story caps rallies. This is the “constructive but unconfirmed” outcome where the supply setup helps at the margin without overpowering a cautious market.

Bear case

In the bear scenario, the halving is revealed as a supply event the market already priced, and TAO behaves as AI-hype beta. The value-capture question stays unanswered, another subnet exit or governance dispute dents confidence the way April’s did, and the broader AI trade rotates out. TAO loses the $200 floor and slides toward the February low near $163 or lower, with the bearish low-end forecasts near $130 coming into view. In this case, the staking lockup offers little protection, because holders unwind positions when yield no longer offsets falling token value, and the thin float that amplifies rallies amplifies declines just as efficiently.

Frequently Asked Questions

When was the Bittensor halving and what changed?

The first Bittensor halving took place on Dec. 12, 2025. Daily TAO emissions were cut in half, from 7,200 tokens to 3,600. The network follows a Bitcoin-style design with a fixed 21 million supply cap, so issuance steps down over time. The supply effect is gradual, filtering into circulating supply over months instead of moving price on the halving date itself.

Does a halving guarantee TAO goes up?

No. A halving reduces the rate of new supply, which can support price if demand holds or grows, but it cannot lift a token on its own. TAO slid toward $200 in the months after the December halving before rebounding, which shows that reduced emissions do not override weak demand or a bearish trend. The halving loads the supply side, but demand has to do the rest.

Why is roughly 70% of TAO staked, and why does it matter?

Holders stake TAO to help secure the network through validators and delegators, and they earn an annual yield around 10% for doing so. Staked tokens are locked and not readily available to sell, which thins the liquid float. Combined with halved emissions, the high staking ratio is the core of the supply-shock argument, since it shrinks the genuinely sellable supply.

What is the biggest risk to the TAO forecast?

The biggest risk is that TAO is valued mostly on AI-narrative momentum instead of durable demand for its subnets. The subnet ecosystem generates revenue, but how much value flows back to the TAO token is unproven, and a high-profile subnet exit in April 2026 triggered a roughly 25% drop. If the AI trade cools or governance fragility resurfaces, the supply setup will not protect the price.

Could a spot TAO ETF change the picture?

Possibly. Grayscale’s Bittensor Trust is already live over the counter, Grayscale filed an S-1, and Bitwise has filed for a spot product, with a U.S. decision expected around August 2026. A favorable outcome would open a regulated channel for institutional capital into a thin float, which the bull case leans on. Approval and timing are not guaranteed, so it remains a catalyst to watch instead of a certainty.

Where do analysts think TAO could trade in 2026?

Third-party forecasts span a wide range. Cautious models such as Gate center near a $236 average with a low around $130, while higher views from Changelly and Cryptopolitan point to averages around $400 to $475 and Coinpedia flags a possible $500 reclaim if key resistance breaks. Long-term 2030 projections from several firms cluster between $900 and $3,000. The spread reflects genuine uncertainty about subnet demand, ETF flows, and the AI trade.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and price predictions are speculative estimates that may not occur. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of June 30, 2026, and will change.

Leave feedback about this